A couple of years ago, my only source of income was from my job and living off pay check by pay check. It only dawn onto me that this is not effective when my peers started getting retrenched and was unable to find a job to replace their income. It didn’t help many did not have emergency funds to tap into. Gone were the days where have a job means security and this is also true for women who solely depend on their husband for allowances. It is essential to have multiple source of income, not only for financial security but also for your own sanity. I have seen many relationships strained because of the sudden change in lifestyle due to retrenchment or women completely lost when their husband decides to leave them and that was their only source of income.

Creating several source of income is not rocket science, yet it is not a ‘1 size fit all’ solution. You want to find those that suit your interests and personality, which is the best way to keep you going for the long haul. 1. Sell products online This can be as simple as selling your pre-loved clothes or items online on platform such as Carousell, E-bay, Craiglist and etc. Statistics has shown that an average person has $5000 worth of unused items are home sitting around. 2. Affiliate marketing Have a book you enjoy or product you have confidence in? Many of these have affiliate programs which enables you advertise them on your website. When a user makes a purchase via a link from your website, you get a cut. 3. Start a freelance project Are you good at creating websites or are skilled in graphic designing? Pick up freelance project from sites such as Fivver on the side. 4. Sign up for OCBC 360/ UOB OB One Accounts / Bank of China SmartSaver If you do not have one of these accounts, get one ASAP! The yearly accumulated interest is as high as 3.55% which is better and some fixed deposit schemes in the market 5. Pick up a part time job Pick up a shift at your nearby super-market or retail place at your down time. Most of us spend weekends lazing at home when we can spend a couple more hours earning the extra cash. Hours in front of the TV dulls the mind, being out sharpens it. 6. Drive Uber or Grab taxi Sign up as driver with Uber start picking up passengers on your way to work or back. The extra buck daily can stretch a long way and these programs have competitive incentives if you hit their commission targets. One driver I spoke to comment that the extra commission can go as high as $1000 extra on top of what his is already earning. 7. Start investing Get into the habit of putting aside a portion of your income and start investing in index funds. The average returns in for Singapore STI is between 4-7% annual including dividends and S&P 500 averages between 8-12% annually. If you are beginner and wish to learn more about investment, I highly recommend Tony Robbin’s book Money: Master The Game (you can purchase them from Amazon) or his upcoming book Unshakable. I started investment about 1.5 years back and my current portfolio is at about 8-9% returns, not too bad for a rookie. 8. Coaching/ Teaching Do you have a skill or hobbies that you are good at? You might want to consider coaching or teaching on the side. Teaching swimming or piano 1 -2 times a week might be a good way to earn that extra income. 9. Real estate In Singapore, it is considered illegal to rent out your place via Air Bnb (unless it is rented out for more than 6 months or if you own a landed property). Therefore most locals buy a SOHO condo or lease out 1 room in their apartments to make additional income. If you are residing outside of Singapore, rent your apartment via Air BnB might be a good source of additional income. There are many other ways to create other sources of income. At the end of the day, find a few that you are interested in and put in a bit of work. A few extra hundred bucks a month can go a long way.

0 Comments

“We are all screwed for 2017!” says a friend of mine during our Christmas gathering as we were discussing what everyone thinks about the coming year. His probably not the only one, talk to any economist or hedge fund managers and ask what they think of 2017, you will get mixed forecast. Truth be told, no one really knows what the future holds. As regular women (and men), we can only take historical data to give us a sense of how the economy will be. While most sees it a dark picture, I personally sees it as an opportunity. If it crashes...great! Since I am already practicing dollar averaging it just means I get to buy more shares with the same amount of money. If the market goes up, even better! I get the chance to rebalance my portfolio either by selling of the portion that is doing well and reinvesting them to the portfolio that is weaker. I know the above can sound a little technical, I will break it down in my posts to come. Before I address the above, I feel it is important my readers get something right in the New Year – Mindset Let’s do a simple check list, are you:

Super-Awesome-Simple-Fundamentals 1 - Pay yourself first Every month your pay cheque comes in and you pay your bills, mortgage, give allowances to your parents (you get the idea) then finally you use what is left over for your own expenses. Hopefully by the end of the month you have leftovers in the bank to buy yourself that extra something. Let’s swap this around and rewire this concept. THE FIRST PERSON YOU PAY IS YOURSELF. Commit a percentage of your salary from 1st January 2017 towards to your investment chest, 5-10% will be a good start if you feel money is tight at this moment. The simplest way is to set up a Giro account and it auto transfer that 5-10% into a separate account. I started doing this when I made my first job and bit by bit it become 50% (again... I am a little crazy; most people are around the 20-30% range eventually). This was also how after 5 years I accumulated small sum money to start my business and my investment portfolio. This concept came when I started reading ‘Think and Grow Rich’ by Napoleon Hills. I manage to find a free online source for this book (click on the link above) and do encourage you to read this as a start, many successful millionaires swears by this book  Super-Awesome-Simple-Fundamentals 2 – Save your wallet, Save the environment Are you one of those that buys 1 cup of Starbucks before going to your office? Or maybe one of the people that buys bottled water because carrying your own bottle is ‘too heavy’ or it is too much of a hassle? Time to kick that habit and here is why: Assuming you buy Starbucks everyday you are working, that’s 260 weekdays. 260 weekdays X $4.90 (Grande Latte) = $1274.00 Or, if you buys 4 X 250ml of bottled drinks daily. 260 weekdays X (4 X $1) = $1040.00 That is alone can take you for a long weekend trip to Thailand or if you are a New Women and invest this amount with 10% interest annually, in 20 years time it will compound to $8570.83 – this is almost 7 times the amount! So the next time you walk into that provision shop or Starbucks, think about how far that dollar can stretch if you made a wiser choice. Let’s just say I started bringing my own water bottle the day I discovered this simple fundamental. Apart from that you might just be doing your part to save the environment, check out a recent article by Channel News Asia on our $134 million bottle water addiction (article link). The amount of pollution from plastic bottles in our world is unprecedented; as New Women, let’s do our part to take care of our planet and our wallets along the way – it’s a straight up win-win situation. There are many other ways to cut back; bringing bottle water or swap your Starbucks for a substitute is the simplest way to get started. The idea is to cut down in small things you are spending on without you noticing.  Super-Awesome-Simple- Fundamentals 3 – Track you expenses I briefly mentioned this in our previous post about tracking your expenses. This is important as the report tells you where your money if going to and where you can increase or decrease your spending. The chart below is a report by Dollar and Sense; it highlights the average income spending of a Singapore house hold (the average household size is 3.3 people per household)  That is about $1,431.51 a person; think about where you can save if this is your household/ individual spending.

Here it is! Start 2017 with 3 good habits:

Many of us hold a job and that is our only source of income. On a weekly basis, we pay a visit to Singapore Pool (state lottery) and pray to the Gods that a win-fall will come and solve all the money problems in our world. In short - we are not in control and allow external forces to determine how we feel about money. A year ago, after struggling with my young business and not having a fixed salary (try it, it will freak the hell out of you if you have been working in a 9-5 job), I had enough of this sucky feeling. ENOUGH! There has to be a way where we can be free of this anxiety and be in control of how we feel about money. Didn't we create an economical system to serves us instead of becoming a slave to it? I started researching and talking to people who has successfully attained the elusive 'financial independence'. That was when my obsessive reading begun and a new state of awareness about money started. Master your relationship with money - New state of awareness Money is NOT a means to an end. It is a great tool to help you achieve your goals and the lifestyle that you want but it is not the ultimate journey. Here is ther kicker *Spoiler Alert*, you will NOT find true happiness even if you achieve your monetary goals. *Shock waves in the room and gasping of air from the audiences*. Yes, I've been there and let me illustrate why. For those who have been working for a few years, think about this; when we all started our career fresh out of school, in our little heads we thought - won't it be great if I earn $xxxx amount and I will be happy? When I first started in my job, that number was $4000 monthly. Within 2 years I hit that mark and the exclude bonuses and guess how I felt? It felt great! For like a couple of days and after that I was back to my regular routine. The feeling didn’t last long and I am back by the run mill in no time, aiming at the next goal or the next promotion. It is good to have goals, it pushes you to be better but just remember at the end of the money rainbow, it is really only just a pot of paper. It takes more important factors such as love, contribution, gratitude, relationships, growth and etc in your life to make your happy. Hold yourself accountable - Accountability is the glue that holds committment to results Do you always blame external factors for your lack of money? A hospital bill, a family member in need of money, someone's wedding, high mortgage and the list goes on. It is time we stop giving excuses and 'men-up' (in our case, women-up) and learn to make smart decisions.

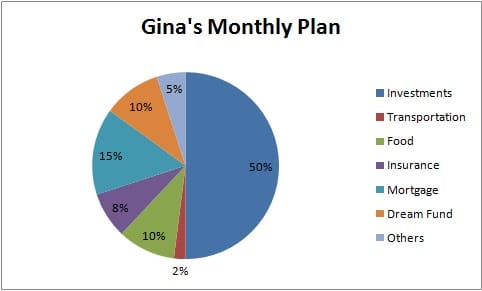

Plan your financials - A goal without a plan is just a wish Pen down how much you are spending on a monthly basis. There are apps for that now and many of them are free. From this data you can start putting them into different chests and plan where everything goes. Below is my monthly plan, my investments chest is more aggressive as I am working on an early financial retirement plan. You have to figure out a ratio that is comfortable for you, bear in mind that I did not start off with 50% investment chest straight away. I sold my car a year ago and found that public transport saves me a ton of money! The difference I saved is channelled to my investment fund and within a year I clocked up close to $50,000 in investments... how crazy is that!  Discipline - The more discipline you become, the easier life gets

Reaching financial independence takes a good routine and repetition until the goal is reached. That means you need to commit to it and this is the part where many of us fall off the wagon. When I decide to commit 50% of my income to investments that means my bonuses or side income from other sources, I make sure half goes to this pot. If there are months that I earn less, I cut expenses at other areas to make this 50% happen. It sounds daunting at first but it gets easier once the momentum kicks in. I reached a point where it becomes enjoyable to see that pot growing because it means I am closer to my goal of financial freedom. Dream Fund - While working hard for the future, girls gotta want to have fun! Its not all boring and gloomy and your mind has to enjoy the process, having a Dream fund is part of the re-wiring. This fund is where you go for your trips, buy the bag you have been eyeing for a long time, donate to a charitable clause or even a gift for your spouse that you know he/she will appreciate. Through this your mind will see this process as enjoyable because you still get to enjoy and feel good as you are working towards your ultimate goal. As it is, I am using this dream fund for Adele's concert in Australia in 2017! It is going to be an exciting journey ahead. Start working on your chest, stick to it and rewire your relationship with money gradually. 10 years down the road, you will thank yourself today for taking that first step. It's only been a year and I am grateful to 'the year ago me' for getting started! |

Author"Earn more, spend less, invest the difference." Archives

February 2017

Categories |

RSS Feed

RSS Feed